The State Pension forms an important part of your retirement income. Although you’ll likely have personal pensions to draw from, the payments from the State Pension are a useful supplement.

You can currently access the State Pension from 66, and this is rising to 67 between April 2026 and 2028. However, you don’t necessarily need to take your State Pension right away. You can choose to delay the payments, as many Brits do each year.

Almost 42,000 people claimed a delayed State Pension in 2023/24

You may assume that most people take their State Pension as soon as they’re able to, but this isn’t true for everybody.

Figures from Royal London show that, in 2023/24, almost 42,000 people started claiming a delayed State Pension. The data also revealed that one in four had postponed their payments for five years or more.

Surprisingly, 591 people still hadn’t started taking their State Pension, even though they had been eligible for more than 20 years.

While delaying for this long might not be beneficial, holding off for a few years could have advantages.

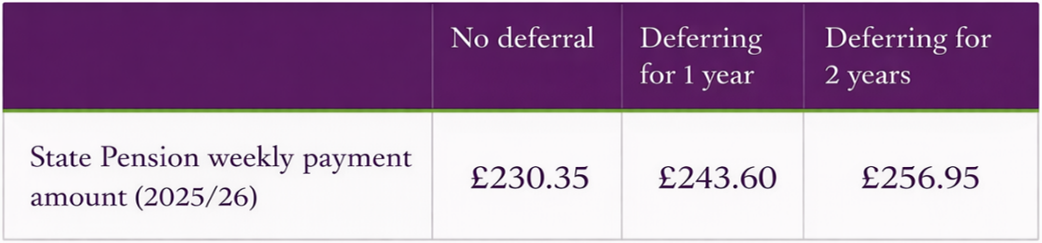

Your State Pension payment increases by 1% for every nine weeks that you defer

When you delay your State Pension, the amount you receive when you eventually do draw the payments increases.

The amount rises by 1% for every nine weeks that you defer.

If you defer for a year or less, you could take the additional funds as a single lump sum payment (known as an arrears payment). For instance, according to the UK government, if you deferred for 52 weeks, you could take an arrears payment of £11,973.

Alternatively, you can increase your weekly State Pension payments by a certain amount, depending on how long you defer for.

Source: UK government

While these figures demonstrate the effects of deferring, the exact amounts will likely change as the State Pension payment rises each year in line with the triple lock.

You can also opt for a combination of an arrears payment and increased regular payments if you defer for more than a year.

For example, if you deferred for 18 months, you could get an arrears payment of £11,973 for the missed payments during the first 12 months. For the remaining 6 months, you would then receive an extra £6.65 a week on your State Pension payments.

As you can see, deferring your State Pension for a few years could increase your regular payments. This may be a useful way to boost your income in retirement, especially if you don’t need the funds when you first reach State Pension Age.

Deferring your State Pension could help you manage your Income Tax liability

When planning your retirement income, you might combine funds from several sources, including personal pensions, State Pension payments, ISAs, and other savings and investments.

It’s important to consider the tax you might pay on these various sources of income.

The first 25% you take from your personal pension is typically tax-free. Any withdrawals from the remaining 75% are subject to Income Tax, as are all your State Pension payments. Meanwhile, funds from your ISAs are tax-free.

The following table shows the rate of Income Tax you could pay on different levels of income.

As you can see, taking the full new State Pension payment of £11,973 a year uses the majority of your tax-free Personal Allowance. If you then made withdrawals from the taxable portion of your pension, you may start paying Income Tax.

In comparison, if you used the tax-free lump sum from your pensions and funds from an ISA, you could be more likely to remain within your Personal Allowance and wouldn’t pay Income Tax.

If you plan your retirement income carefully and only take what you need to cover your living costs, rather than drawing the State Pension immediately, you could reduce the amount of Income Tax you pay each year.

While you may still pay some Income Tax, particularly later in retirement when you’ve used your tax-free lump sum, you could reduce the amount by being mindful about how and when you access the State Pension.

It takes more than 15 years to earn back a year’s worth of deferred State Pension payments

Although deferring your State Pension could increase the amount you receive later, it may only be worthwhile if you live long enough to recoup the lost income.

For instance, if you delay your payments for a year, you’ll miss out on £11,973.

According to the UK government, it will take more than 15 years of increased payments to earn this amount back. You will continue receiving the increased payments after this. This is less of an issue if you only delay for one year, as you can receive an arrears payment for the full amount.

However, if you defer for more than one year, you may have to live for a long time before you reach a “break-even point” and your increased payments exceed the amount you missed out on by delaying.

Bear in mind that if you defer for several years, your break-even point could be much longer, and you’ll need to factor this in when making your decision.

Get in touch

Deferring your State Pension payments may benefit you by increasing your retirement income later, but there are challenges to consider. We can review your unique situation and explore retirement income options to help you make the right decision.

Please contact us at hello@ardentuk.com or call or WhatsApp us on 01904 655 330. As an award-winning financial advice company with advisers included in the 2025 VouchedFor Top Rated guide, we can assure you that we’re a bona fide company providing excellent advice and high-quality service.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation, and regulation, which are subject to change in the future.